Materiality

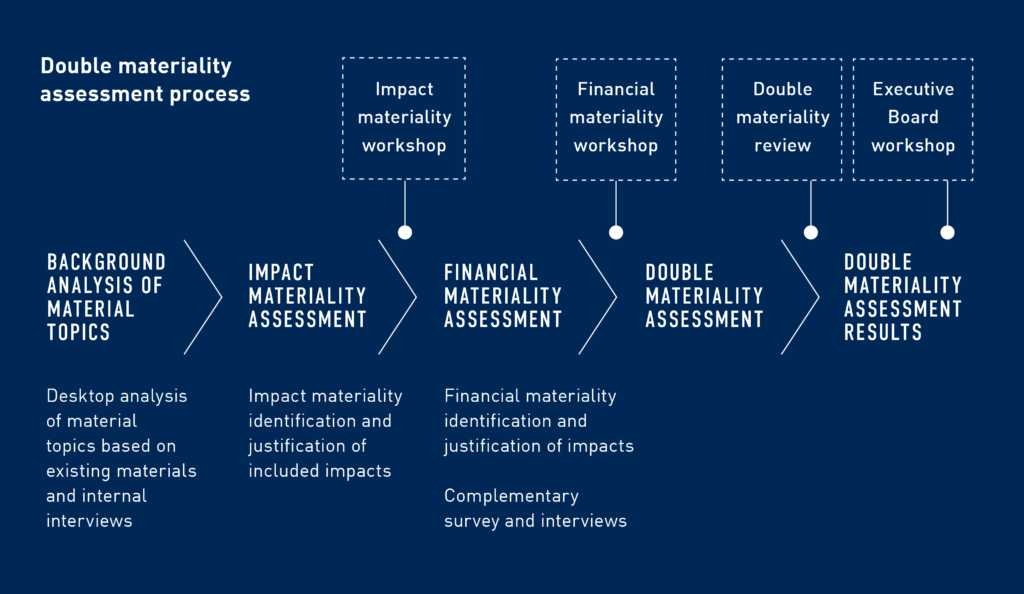

In 2025, we conducted a review for double materiality assessment (DMA) to prepare for the ESRS reporting.

The DMA confirmed the most material sustainability topics for Amer Sports and provided key insights to shape our sustainability strategy. It identified both the outward impacts of our business on people and the environment, and the inward risks and opportunities that sustainability factors present to our business model. The DMA conducted in 2023, has been used in the sustainability report 2024.

The assessment covered the entire Amer Sports value chain, spanning both our own activities and those in the upstream and downstream segments. It included two perspectives:

• Impact materiality: What impacts does our business have on people and the environment?

• Financial materiality: What are the Environmental, Social, and Governance (ESG)-related business risks and opportunities that have a financial impact on our business?

The Amer Sports double materiality process

The assessment was conducted in four phases:

1) value chain mapping

2) impact assessment

3) financial assessment (risks & opportunities)

4) determination.

As a result of the assessment, seven material topics, with the identified sub-topics in line with European Sustainability Reporting Standards (ESRS) were identified to be material to Amer Sports’ business and defined for reporting. E1 Climate Change, E5 Circular Economy and S4 Consumers and end-users were assessed as high of impact materiality and high of financial materiality. S2 Workers in the value chain was assessed high of impact materiality and moderate of financial materiality, while E2 Pollution and S1 Own workforce and G1 Business conduct were assessed high of impact materiality and low of financial materiality.

This assessment identified key drivers in our value chain – both upstream and downstream – covering impact, risks, and opportunities. Used scoring methodology incorporates severity and likelihood for impact materiality and magnitude and likelihood for financial materiality with the scale of 0-5 for impact, risks and opportunities.

Material topics

- E1 Climate change

- E2 Pollution

- E5 Circular economy

- S2 Workers in the value chain

- S4 Consumers and end-users

- S1 Own workforce

- G1 Business conduct